In response to the pandemic, the IRS moved the federal income tax filing deadline back three months from April 15 to July 15. The July 15 deadline applies to:

Filing income tax returns

Payment of income taxes due

Payment of estimated taxes due for the first quarter of 2020

Funding retirement account contributions for 2019

Funding Health Savings Account contributions for 2019

In addition, this 3-month period will be disregarded for calculating interest, penalties, and additional taxes for failure to file returns or pay taxes.

The new deadline applies to individuals, trusts, estates, partnerships, associations, and companies and corporations.

For California residents, the Franchise Tax Board also extended tax deadlines to July 15. You can delay filing and payment of taxes (including second and first quarter estimated payments), LLC taxes and fees, and non-wage withholding payments. California is also waiving interest and penalties for individuals and businesses.

Taxpayers that are entitled to a refund.

You are encouraged to file as soon as possible in order to get your refund more quickly.

Platt Wealth Management offers financial plans to answer your important financial questions. Where are you? Where do you want to be? How can you get there? Our four-step financial planning process is designed to be a road map to get you where you want to go while providing flexibility to adapt to changes along the route. We offer stand alone plans or full wealth management plans that include our investment management services. Give us a call today to set up a complimentary review. 619-255-9554.

So, the Federal Reserve Bank lowered interest rates to a range of 0% to 0.25%. Why aren’t mortgage rates following? Well, time to dust off that old college economics book. Let’s answer that by following the chain of economic reactions to the Fed’s actions and the principals of supply and demand.

How is the benchmark federal funds rate related to mortgage rates?

The rate that the Fed cut is the benchmark federal funds rate. This is the short-term interest rate banks charge other banks for overnight lending and borrowing. So, bank to bank loan deals.

The Fed dropped this rate on March 15 for the second time in 2020 in response to the economic disruption caused by the Coronavirus. When the target federal funds rate decreases, banks typically follow by lowering their prime interest rates. The prime interest rate is used to set variable interest rates.

So, that new credit card application you just got in the mail might have a lower rate than your current credit card. Lowering the prime rate will cause other consumer interest rates tied to the prime rate to decrease as well. Businesses will have access to short term loans with lower interest rates to help with cash flow needs.

How does the federal funds rate and prime rate affect mortgage rates?

Mortgage rates are different from other consumer interest rates. Generally, mortgages rates don’t track the Fed’s movements. Mortgage rates are long-term loans, versus the short term variable rate we talked about earlier. So mortgage rates will go up or down depending on long term bond yields. The bond market exerts more influence over mortgage rates, not the Fed.

When the stock market falls, investors flee to government bonds for safety and stability. When the demand for bonds goes up, the price of bonds goes up. Bond prices and yield/interest rates have an inverse relationship. So, when bond prices go up, interest rates go down. Mortgage bonds are the same. When demand for mortgage bonds goes up, mortgage rates go down.

When will mortgage rates drop?

Early in March, mortgage rates dropped because the demand for long-term mortgage bonds was high. In response to low mortgage rates, the market was flooded by consumers looking to refinance. The supply of mortgage bonds increased and the demand for mortgage bonds dropped. Within a week or two, mortgage rates rose quickly.

The Fed is using other tools in their arsenal to cushion the economy, including buying Treasuries and mortgage-backed securities. As the demand for mortgage bonds grows, mortgage rates will come down again. However, consumers aren’t likely to see 0% mortgage rates. Mortgage bonds are considered riskier than government bonds. Interest rates are higher to compensate for the additional risk banks take in making the loans.

If you are looking to refinance your current mortgage or buy a house, keep your eyes on the rates. Be ready to go when rates dip. Be aware that you won’t be the only one refinancing when rates are attractive. Mortgage brokers will be busy and lock-in periods of 60 to 90 days (or even longer) are becoming more common.

Platt Wealth Management offers financial plans to answer your important financial questions. Where are you? Where do you want to be? How can you get there? Our four-step financial planning process is designed to be a road map to get you where you want to go while providing flexibility to adapt to changes along the route. We offer stand alone plans or full wealth management plans that include our investment management services. Give us a call today to set up a complimentary review. 619-255-9554.

Investing during an election year can be tough on the nerves. 2020 promises to be no different. Politics can bring out strong emotions and biases. Investors would be wise to put these aside when making investment decisions.

Benjamin Graham, the father of value investing, famously noted that “In the short run, the market is a voting machine but in the long run, it is a weighing machine.” He wasn’t literally referring to the intersection of elections and investing, but he could have been. Markets can be especially choppy during election years. Sentiment often changes as quickly as candidates open their mouths.

Graham first made his analogy in 1934, in his seminal book, “Security Analysis.” Since then there have been 22 election cycles. We’ve analyzed them all to help you prepare for investing in these potentially volatile periods. Below we highlight three common mistakes made by investors in election years and offer ways to avoid these pitfalls and invest with confidence in 2020.

Mistake #1: Investors worry too much about which party wins the election

There’s nothing wrong with wanting your candidate to win. Investors run into trouble when they place too much importance on election results. That’s because elections have, historically speaking, made essentially no difference when it comes to long-term investment returns.

“Presidents get far too much credit, and far too much blame, for the health of the U.S. economy and the state of the financial markets,” says economist Darrell Spence. “There are many other variables that determine economic growth and market returns and, frankly, presidents have very little influence over them.”

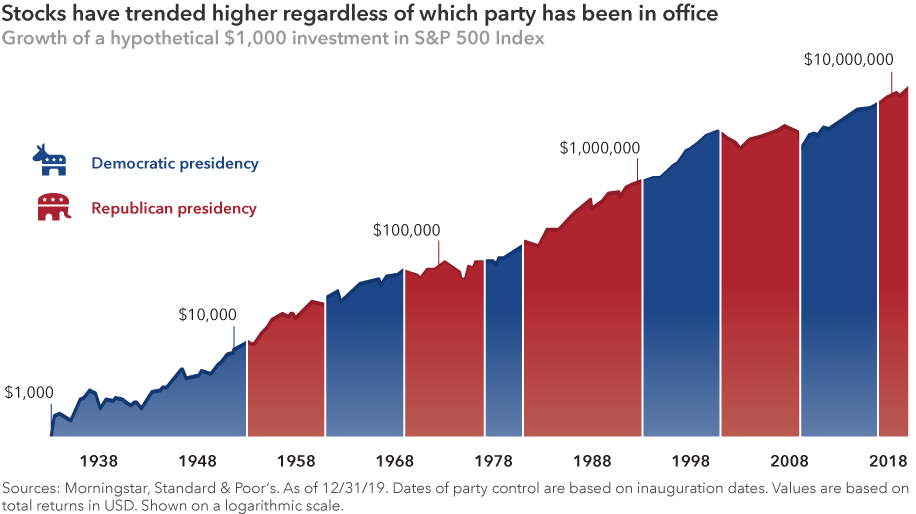

What should matter more to investors is staying invested. Although past results are not predictive of future returns, a $1,000 investment in the S&P 500 made when Franklin D. Roosevelt took office would have been worth over $14 million today. During this time there have been exactly seven Democratic and seven Republican presidents. Getting out of the market to avoid a certain party or candidate in office could have severely detracted from an investor’s long-term returns.

By design, elections have clear winners and losers. But the real winners were investors who avoided the temptation to base their decisions around election results and stayed invested for the long haul.

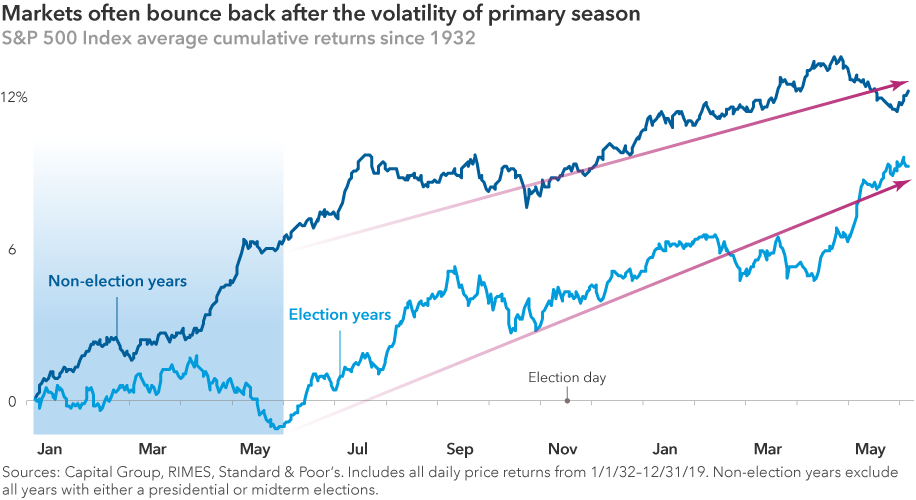

Mistake #2: Investors get spooked by primary season volatility

Markets hate uncertainty, and what’s more uncertain than primary season of an election year? With so many candidates on the campaign trail — 11 Democrats were still running when primaries kicked off in early February — the range of outcomes can feel daunting.

But volatility caused by this uncertainty is often short-lived. After the primaries are over and each party has selected its candidate, markets have tended to return to their normal upward trajectory.

Election year volatility can also bring select buying opportunities. Policy proposals during primaries often target specific industries, putting pressure on share prices. This cycle, it’s the health care sector that’s in the spotlight as several candidates have proposed overhauls to drug pricing and the health care system.

Does that mean you should avoid this sector altogether? Not according to Rob Lovelace, an equity manager with 34 years of experience investing through many election cycles. “When everyone is worried that a new government policy is going to come along and destroy a sector, that concern is usually overblown,” Lovelace says. “Companies with good drugs that are really helping people will be able to get into the market, and they will get paid for it.”

In the past, those targeted sectors have often rallied after the campaign spotlight dimmed. It happened with health care following the 2016 presidential and 2018 midterm elections. This has happened with other sectors in the past. This can create buying opportunities for investors with a contrarian point of view and the ability to withstand short-term volatility.

Mistake #3: Investors try to time the markets around politics

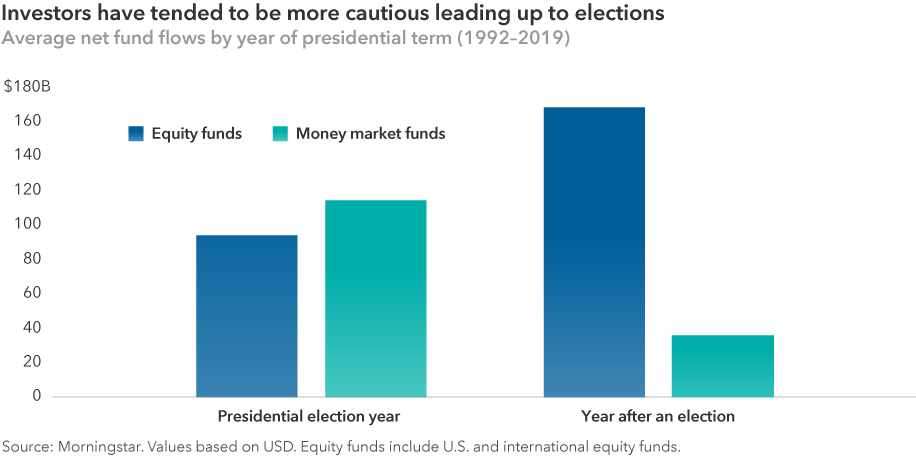

If you’re nervous about the markets in 2020, you’re not alone. Presidential candidates often draw attention to the country’s problems, and campaigns regularly amplify negative messages. So maybe it should be no surprise that investors have tended to be more conservative with their portfolios ahead of elections.

Since 1992, investors have poured assets into money market funds — traditionally one of the lowest risk investment vehicles — much more often leading up to elections. By contrast, equity funds have seen the highest net inflows in the year immediately after an election. This suggests that investors may prefer to minimize risk during election years and wait until after uncertainty has subsided to revisit riskier assets like stocks.

But market timing is rarely a winning long-term investment strategy. It can pose a major problem for portfolio returns. To verify this, we analyzed investment returns over the last 22 election cycles to compare three hypothetical investment approaches: being fully invested in equities, making monthly contributions to equities, or staying in cash until after the election. We then calculated the portfolio returns after each cycle, assuming a four-year holding period.

The hypothetical investor who stayed in cash until after the election had the worst outcome of the three portfolios in 16 of 22 periods. Meanwhile, investors who were fully invested or made monthly contributions during election years came out on top. These investors had higher average portfolio balances over the full period and more often outpaced the investor who stayed on the sidelines longer.

Sticking with a sound long-term investment plan based on individual investment objectives is usually the best course of action. Whether that strategy is to be fully invested throughout the year or to consistently invest through a vehicle such as a 401(k) plan, the bottom line is that investors should avoid market timing around politics. As is often the case with investing, the key is to put aside short-term noise and focus on long-term goals.

How can investors avoid these mistakes?

Don’t allow election predictions and outcomes to influence investment decisions. History shows that election results have very little impact on long-term returns.

Expect volatility, especially during primary season, but don’t fear it. View it as a potential opportunity.

Stick to a long-term investment strategy instead of trying to time markets around elections. Investors who were fully invested or made regular, monthly investments did better than those who stayed in cash in election years.

As Chinese authorities deal with a rapidly spreading coronavirus, investors are raising questions about the potential impact on global economic growth and the financial markets. While much is still unknown about the extent of the outbreak — and, crucially, how long it may last — the initial drag on China and other emerging markets is starting to come into focus.

China’s Economy and the Coronavirus Outbreak

China’s economy was already growing at the slowest rate in 30 years before reports of the outbreak first emerged in the central China city of Wuhan. Since then, the Chinese government has placed a dozen cities under quarantine, shut down businesses and schools, and restricted travel in the affected regions. More than 7,700 infections have been reported as of January 30, including a small number in the U.S., Europe and other parts of Asia.

To get a handle on how the outbreak is affecting global economic conditions, we talked to two Capital Group investment veterans who are based in Hong Kong, as well as one of our U.S. economists. Here’s a look at their perspectives:

“Given the quarantine lockdowns, it’s highly likely that the numbers of infected people in mainland China are significantly underestimated,” says Stephen Green, a Capital Group economist based in Hong Kong, “especially in rural areas where medical facilities are limited.

“Depending on how long it takes to contain the coronavirus, we should expect to see sizable declines in consumer spending and manufacturing activity at least through the end of February,” Green adds. “I wouldn’t be surprised if China’s first-quarter GDP growth falls below 6% and some Wall Street estimates are as low as 5%, which is certainly in the realm of possibility.”

A Global Slowdown from the Coronavirus Outbreak

Outside China, the biggest economic impact is expected to be in Thailand, which relies heavily on Chinese tourism. Among industries, travel and tourism throughout Asia will likely take a significant hit, Green explains, along with sales of luxury goods. In addition, many events associated with China’s lunar new year have been canceled. Energy stocks also have fallen sharply as investors expect oil prices to decline further amid lower demand from China.

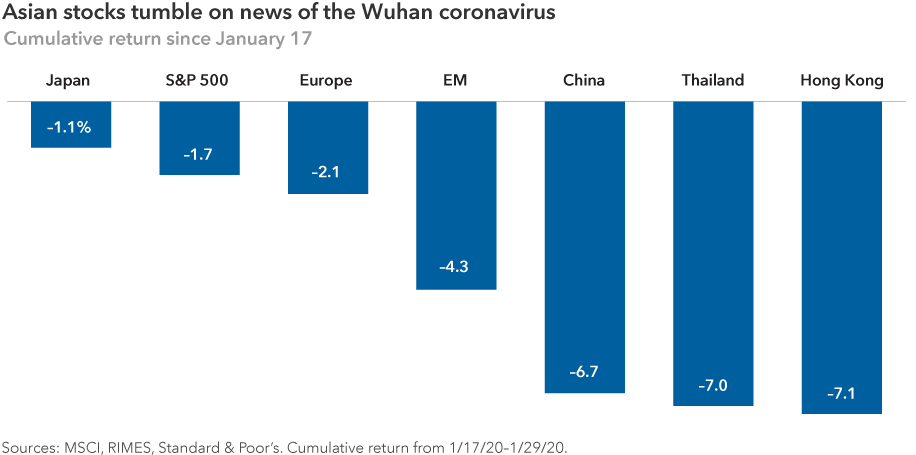

Since news reports about the virus accelerated around January 17, emerging markets stocks have declined by about 4%, as measured by the MSCI Emerging Markets IMI. Chinese stocks are down more than 6% and Thai stocks slipped 7%. By comparison, the MSCI World Index declined 1.3% during the period through January 29.

If the economy and markets continue to deteriorate, Green notes, Chinese authorities are likely to launch new stimulus measures, including potential tax cuts and interest rate cuts.

How will the US economy be affected by the Coronavirus Outbreak?

U.S. stocks, meanwhile, have lost about 2% on worries that the outbreak could have a spillover effect on the U.S. economy, including American companies that do business in China. Starbucks has closed about half of its 4,300 stores in China. Many U.S.-based airlines are also canceling flights to the country. And there are growing concerns about supply-chain disruptions for companies such as Apple that have significant manufacturing operations there.

Coupled with Boeing’s recent troubles returning the 737 Max jet to service, the outlook for the U.S. economy now looks more uncertain than it did just a few weeks ago, says Capital Group U.S. economist Jared Franz. Fourth-quarter U.S. GDP growth came in at 2.1% on an annualized basis, according to Commerce Department figures released on Thursday

“If 737 Max production remains grounded through July, then I estimate the impact on first-half GDP growth will be roughly –0.5 percentage points,” Franz says. “The economic impact of the coronavirus on the U.S. is more difficult to calibrate, but I expect it to be modest and mostly felt through trade disruption and financial linkages.”

Assuming the outbreak is contained soon, Franz said it’s likely global economic growth will experience a V-shaped recovery characterized by slower growth in the first half and a significant acceleration in the second half of the year. The U.S. economy will probably follow the same course.

“U.S. economic fundamentals remain sound, labor markets are resilient and the Federal Reserve stands ready to take action as needed,” Franz adds. “The coronavirus looks to be a modest but temporary restraint on U.S. economic activity via secondary channels of impact, but should not derail my growth expectations of roughly 2% in 2020.”

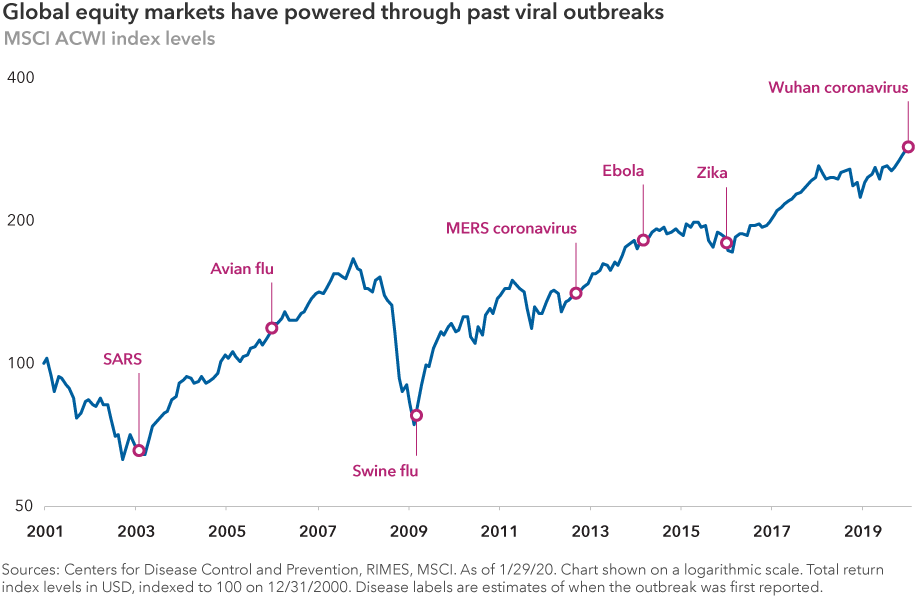

Coronavirus Outbreak Compared to SARS

That’s similar to the pattern shown after the SARS outbreak that hit China in 2002 and 2003. Key indicators bounced back quickly after the virus was contained. Many investors are looking at the SARS event as a template for what might happen in the weeks and months ahead — although it’s important to note that there were many other factors during that time period, including the aftermath of the 9/11 attacks and the U.S. invasion of Iraq in 2003.

In addition, the structure of the global economy was significantly different. The Chinese economy was largely investment-driven at that time. Consumer spending is a much larger percentage of total economic output today. Travel and tourism activity also was much lower than it is now, with Chinese tourism skyrocketing over the past decade.

Investment Implications

That’s similar to the pattern shown after the SARS outbreak that hit China in 2002 and 2003. Key indicators bounced back quickly after the virus was contained. Many investors are looking at the SARS event as a template for what might happen in the weeks and months ahead — although it’s important to note that there were many other factors during that time period, including the aftermath of the 9/11 attacks and the U.S. invasion of Iraq in 2003.

In addition, the structure of the global economy was significantly different. The Chinese economy was largely investment-driven at that time. Consumer spending is a much larger percentage of total economic output today. Travel and tourism activity also was much lower than it is now, with Chinese tourism skyrocketing over the past decade.

That said, market psychology is often highly predictable during times of crisis as investors tend to overreact to distressing news, says Steve Watson, a Capital Group portfolio manager based in Hong Kong.

“The situation today is very reminiscent of SARS, which we lived through here in Hong Kong 17 years ago,” Watson explains. “The uncertainty was extremely high during the SARS outbreak and it was certainly a difficult time for many people, but once it was over, the following relief rally was powerful.”

As with any large-scale crisis, long-term investors should look for select opportunities that may be generated by a near-term loss of confidence, Watson says. “This is when long-term thinking, on-the-ground research and a focus on value can make a meaningful difference.”

SECURE Act Brings Big Changes to Retirement Account Rules

President Trump signed the Setting Every Community Up for Retirement Enhancement (SECURE) Act into law on December 20th, 2019. Itbecomes effective as of January 1, 2020. It brings sweeping changes, including a later starting age for Required Minimum Distributions, more opportunities for contributing to IRAs, and the end of the stretch IRA strategy for inherited IRAs. Below are details on some of the key provisions.

The SECURE Act Allows Longer Tax-Deferred Growth for IRAs

RMDs (Required Minimum Distributions) to begin at age 72.If you turn age 70 ½ after December 31, 2019, your required distributions from traditional retirement accounts will begin at age 72 instead of age 70 ½. Unfortunately, if you turned 70 ½ in 2019, you must still take your 2019 RMD no later than April 1, 2020. If you are already taking RMDs because you are over 70 ½, you must continue taking your RMDs.

QCDs (Qualified Charitable Distributions) continue for those over 70 ½

QCDs are direct transfers from your IRA to a qualified charity so that the distribution is excluded from your income. The QCD rule that you must be 70 ½ will remain unchanged even though the age for starting RMDs will increase to 72. There may be an impact to your QCD if you make deductible contributions to your IRA after age 70 ½.

Contributions to IRA accounts allowed after age 70 ½ . Beginning in 2020, if you have earned income, you will now be able to contribute to your traditional IRA without any age limitations. If you are married, your spouse can also contribute to an IRA even if they do not have any earned income.

The SECURE Act Permits Students to Use 529 Money to Pay Back Loans

Expanded use for 529 college savings accounts. The definition of a qualified distribution from a 529 college savings has been expanded to include up to $10,000 to repay qualified student loans and expenses for certain apprenticeship programs. This provision of the SECURE Act is retroactive to distributions made after December 31, 2018.

New Moms and Dads Get Penalty-Free Withdrawals from Retirement Accounts

Penalty-free withdrawals for birth or adoption expenses. Beginning in 2020, parents can withdraw up to $5,000 from a retirement account within one year of the child’s birth or adoption. You will owe taxes on the distribution, but the usual 10% penaltyfor account owners younger than 59 ½ will be waived.

The SECURE Act Eliminates Stretch IRA for Inherited IRA Accounts

Inheritors must take more care with tax planning when taking distributions. There are no changes for anyone who inherited an IRA from the original owner who passed away before January 1, 2020. However, if the original IRA owner passes away after December 31, 2019, most beneficiaries will need to withdraw all assets from the inherited IRA within 10 years following the death of the IRA owner instead of spreading required distributions over their own lifetimes. This provision applies to both traditional and Roth IRA accounts. There are exceptions for spouses, minor children (until they reach the age of majority), disabled individuals, and beneficiaries who are less than 10 years younger than the decedent.

Are you on track for retirement?

Making sure you will be ready for retirement can be overwhelming. Funding your retirement accounts over the years is just one part of your journey to the retirement of your dreams. A Certified Financial PlannerTM can help you navigate the complexities of financial planning. Talk to a Financial Planner>

Platt Wealth Management offers financial plans to answer your important financial questions. Where are you? Where do you want to be? How can you get there? Our four-step financial planning process is designed to be a road map to get you where you want to go while providing flexibility to adapt to changes along the route. We offer stand alone plans or full wealth management plans that include our investment management services. Give us a call today to set up a complimentary review. 619-255-9554.

Higher contribution limits in 2020 mean more retirement savings for you.

If you recently hit 50, you might have realized that your retirement savings is not quite where you want it. You’re not alone. Many people come to us for a financial plan worried that they don’t have enough retirement savings to keep the lifestyle they want in retirement.

Luckily, the IRS seems to know this also and recently announced higher contribution limits for qualified retirement accounts. This can mean more retirement savings for you. Next year, the contribution limits for qualified retirement plans including 401(k)sand 403(b)s are increasingfrom $19,000 to $19,500. If you are 50 or older, the catch-up contribution is also increasing by $500, from $6,000 to $6,500, so you can make a total contribution of $26,000 in pre-tax or Roth contributions. If you are turning 50, you are now eligible to boost retirement savings through catch-up contributions. You can make catch-up contributions at any time during the year that you turn 50 (you don’t have to wait until you actually turn 50).

IRA contribution and catch-up limits are staying at the same levels for 2020, with $6,000 per person, plus an additional $1,000 catch-up contribution for people that are 50 and older.

Are you on track for retirement?

Making sure you will be ready for retirement can be overwhelming. Funding your retirement accounts over the years is just one part of your journey to the retirement of your dreams. A Certified Financial PlannerTM can help you navigate the complexities of financial planning. Talk to a Financial Planner>

Health Savings Accounts

The contribution limits for Health Savings Accounts (HSA) are also increasing. Individuals can contribute $3,550 next year (up $50 from this year), and families can contribute $7,100 (a $100 increase). The catch-up contribution for those age 55 years and older remains at $1,000.

Business Owner Retirement Savings

The limit for SEP IRAs will be $57,000; since SEP IRAs are considered an employer plan, there is no catch-up contribution. SIMPLE IRA limits have increased by $500 from $13,000 to $13,500. The over-50 catch-up contribution remains at $3,000 for 2020, for a total contribution of $16,500.

Platt Wealth Management offers financial plans to answer your important financial questions. Where are you? Where do you want to be? How can you get there? Our four-step financial planning process is designed to be a road map to get you where you want to go while providing flexibility to adapt to changes along the route. We offer stand alone plans or full wealth management plans that include our investment management services. Give us a call today to set up a complimentary review. 619-255-9554.