2022 1st Quarter Review

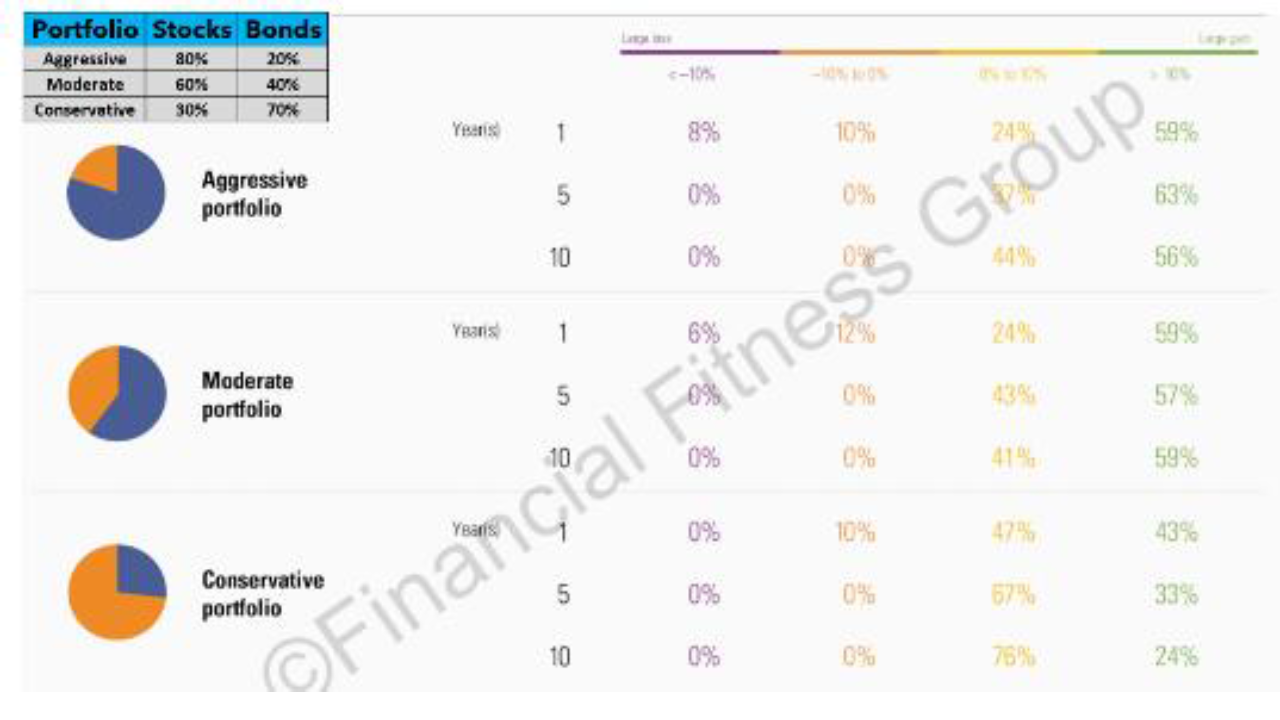

For a Moderate portfolio (60% stock/40% bond allocation) and an Aggressive portfolio (80% stock/20% bond allocation), the probability of a loss over 5-year rolling periods was 0% (same for the Conservative portfolio with a 30% stock/70% bond allocation). There was an 18% chance of a loss over one year for the Moderate and Aggressive portfolios, but usually that loss is less than 10%. The odds are pretty good that over the next 5-years, these portfolios will have positive results, and there is even more than an 80% chance that they will have positive results over the next 12-months. See illustration from Morningstar 2021 below.

WE ARE HERE FOR YOU

The Platt Wealth Management team is here for you to discuss any changes to your financial situation or investment objectives. We are always available to assist you with any financial matters of concern to you and look forward to continuing to serve as your partner along your financial journey.

Warmest regards,

Platt Wealth Management

")